Tracxn Technologies, a leading private markets intelligence provider in India, has released its latest report on India’s startup landscape — as at the end of the fiscal year 2025-26.

Press release

Key highlights

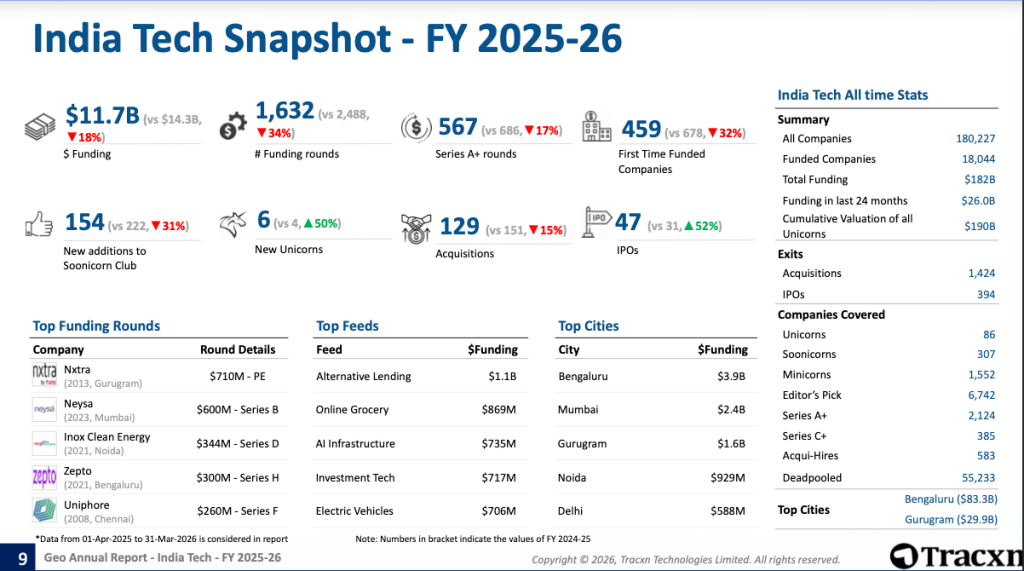

$11.7B raised across 1,632 rounds — deal volume fell 34% but total capital fell only 18%.

Median cheque size grew substantially, confirming that investors are concentrating capital rather than retreating from the market.

Early-stage funding rose 33% to $4.8B even as early-stage rounds fell from 492 to 420.

Fewer companies attracted larger Series A and B rounds — a barometer of rising quality thresholds at the growth stage.

47 IPOs in FY 2025-26, up 52% from 31 the prior year. India’s public markets absorbed the most tech listings in a decade, with Lenskart, Groww, Meesho, Physics Wallah, and Pine Labs among the notable debutants.

Six new unicorns formed in FY 2025-26 — up 50% year-on-year — and reached billion-dollar valuations on an average of $150M raised, nearly half the $294M required by the prior cohort.

74% of India-focused VCs expect conditions to improve in 2026, with AI/ML and Deep Tech as top priorities — and talent shortages, not capital, as the chief execution risk.

Bengaluru, 21st April 2026: Tracxn, a leading startup intelligence and market data platform, today released the Tracxn Geo Annual

Report: India Tech FY 2025-26, providing the most comprehensive data-backed review of India’s startup funding, exits, unicorn formation, and investor activity for the financial year ending 31 March 2026.

India retained its position as the world’s fourth-highest funded startup ecosystem, behind only the United States, United Kingdom, and China, accounting for $11.7B deployed across 1,632

Rounds.

The headline funding figure masks a more important structural story: deal volume compression is running far ahead of funding compression, reflecting an investor base that is making fewer, higher-conviction bets rather than retreating from the market altogether.

Commenting on the insights, Neha Singh, Co-Founder of Tracxn, said, “The FY 2025-26 data tells a story of deliberate recalibration. When deal volume falls 34% but funding fell only 18%, it means investors aren’t leaving — they’re choosing differently. The surge in IPO activity and the 50% rise in new unicorn formation all point to an ecosystem that is growing up: more focused, more fundamentals-driven, and increasingly capable of generating durable value rather than just headline valuations.”

Capital Is Concentrating, Not Retreating

India’s $11.7B represented an 18% decline from $14.3B the prior financial year, but a 20% increase over FY 2023-24’s trough. Early-stage funding grew 33% to $4.8B despite fewer rounds; late-stage fell 38%. Enterprise Applications ($3.6B), FinTech ($2.4B), and Retail ($2.4B) led sectors. The year’s largest rounds — Nxtra ($710M), Neysa ($600M), and Inox Clean Energy ($344M) — signal that India’s most capital-intensive opportunities lie in foundational infrastructure.

Public Markets Come of Age

FY 2025-26 produced 47 tech IPOs — a 52% year-on-year increase and the highest count in the India Tech ecosystem. Notable listings and their respective market capitalisations at the time of IPO included Lenskart ($7.9B), Groww ($7.0B), Meesho ($5.6B), Physics Wallah ($3.6B) — collectively representing some of India’s most prominent VC-backed success stories reaching public scale.

The sector composition of FY 2025-26 IPOs shifted markedly from the prior financial year: Retail led with 15 listings and Enterprise Applications followed with 11, compared to Transportation & Logistics Tech leading in FY 2024-25. Late-stage IPOs rose from 36% to 44% of equity-funded listings, reflecting investor preference for scaled, revenue-generating businesses.

Unicorns: Faster, Leaner, More Capital-Efficient

Six new unicorns emerged in FY 2025-26 — Neysa, Raise, Navi, Jumbotail, JSW One MSME, and Juspay — a 50% increase over the four formed in FY 2024-25. India’s cumulative unicorn count now stands at 125, positioning it as the world’s third-largest unicorn ecosystem. Bengaluru (53) and Mumbai (20) and Gurugram (20) account for over 74% of all unicorns. Of 94 private unicorns with available financials, only 17 are currently profitable, underscoring that margin discipline, not just revenue scale, will define the next phase of the ecosystem.

What India’s Investors Are Signalling for 2026

A survey of ~30 India-focused VC investors found 74% expect conditions to improve in 2026, with AI/ML and Deep Tech tied as top sector priorities (71% each), and Vertical AI (79%) and Enterprise AI (54%) as preferred deployment categories — signalling that the next growth phase will be defined by where intelligence gets embedded, not just deployed.